Gas tax stupid

Verb or noun - you choose!

We’ve all seen the clips, the headlines, the billboards. Apparently Australian gas is given away for free, no tax paid. Gas is even cheaper overseas than it is here and Japan makes more from our gas than we do.

I think that sums up the various angles, if I’ve missed anything let me know.

I only watched a couple of the Senate’s gas tax inquiry sessions – Richard Denniss from the Australia institute and Cecile Wake from Shell. My first impression watching Wake’s refusal to state revenue and volume figures, dutifully captured by the activists and blasted across social media, was she could do better.

And then she did. Wake spent a glorious 6 minutes exposing Australia Institute misinformation on Hansard while Sarah Hanson-Young tried and failed to shut her down.

https://www.aph.gov.au/News_and_Events/Watch_Read_Listen/ParlView/video/4519947

Wake was a highly competitive pentathlete in her younger years and has risen to the top job in Shell Australia. She’s no idiot. By contrast Sarah Hanson-Young is married to the former director of the Australia Institute – Ben Oquist. Inquiry panel member David Pocock’s wife Emma is a former staffer for Hanson-Young and Richard Denniss, current head of the Australia Institute, is a former chief of staff for Bob Brown. The green roots go deep.

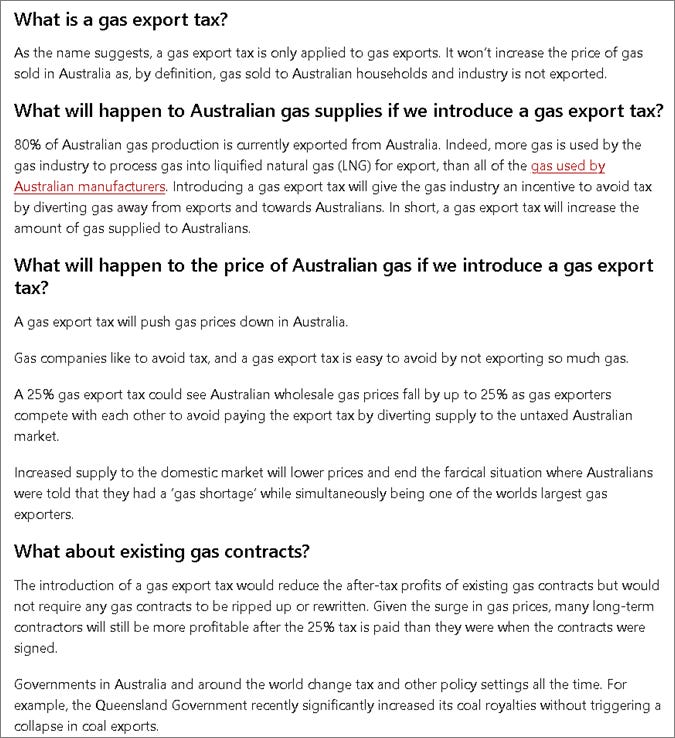

Denniss has helpfully written a ‘gas tax explainer’ and stuck it on the internet for everybody to see. Denniss’ position is that higher taxes will encourage gas producers to redirect export gas to the domestic market resulting in excess supply and lower prices.

In this writeup we’ll examine Denniss’ theory and see if it can work.

Source: https://thepoint.com.au/explainers/260323-the-case-for-a-gas-export-tax-explained

Before we dive into the gas stuff I have to pay some attention to this fabulous example of misdirection. Here’s the full statement:

“Governments in Australia and around the world change tax and other policy settings all the time. For example, the Queensland Government recently significantly increased its coal royalties without triggering a collapse in coal exports.”

I am applying Hitchens’ Razor to the first part i.e. a claim asserted without evidence can be dismissed without evidence.

Governments in Australia and around the world change tax and other policy settings all the time.

Whether they do or not, this is an unsubstantiated assertion. I could just as well make the claim that governments around the world hardly ever make changes to their resource royalty arrangements. Who would be correct? I could even use the often cited Norway as an example of stable tax settings. Could Denniss offer some supporting evidence for his claim? We’ll likely never know.

For example, the Queensland Government recently significantly increased its coal royalties without triggering a collapse in coal exports.

The Queensland government under the short-lived Steven Miles imposed large increases to coal royalties in 2022. By comparison the NSW coal royalty rates consist of flat rates from 8.8% to 10.8% of the sale price.

Impacts of the increased royalty regime will always be debated, but the reality is tough times now for coal miners with several mines either mothballed or closed outright e.g. Cook Colliery (QCoal), Saraji South (BHP Mitsubishi Alliance - BMA), Bluff Mine (Bowen Coking Coal), Burton Complex (Bowen Coking Coal), Wilkie Creek & Mavis Downs, Millennium Mine, Vulcan South (Vitrinite).

Commodity prices and the vagaries of international trade also have significant effects on resource project viability. Is the volume of coal exported even relevant in this context?

The point of this sidebar is to highlight that Denniss’ claim that tax and royalty changes have no effect are laughable. Of course it has an effect. Jobs, investment, raw product – it’s all impacted.

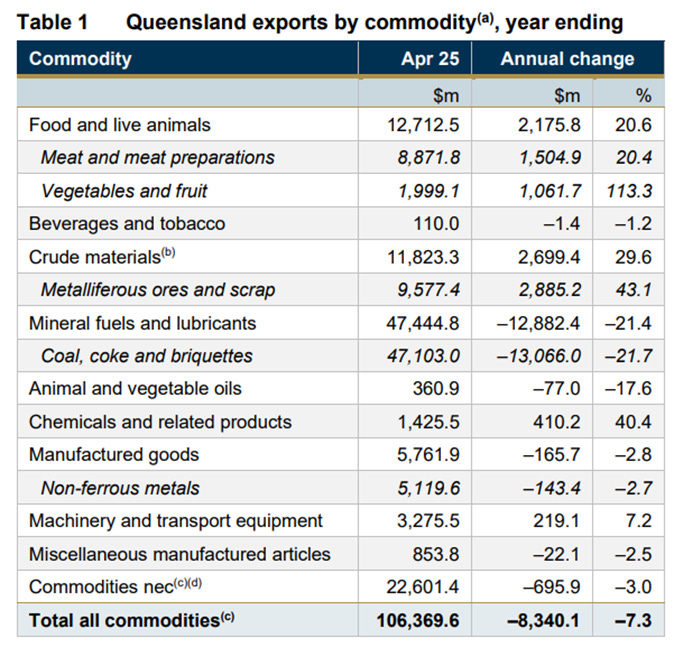

Queensland Treasury data shows some of the changes just in the last year with coal exports down 21.7%, a ‘mere’ $13 billion. No effect Mr Denniss?

Source: https://www.qgso.qld.gov.au/issues/3526/exports-qld-goods-overseas-202504.pdf

For more on the Queensland coal royalty debacle I recommend two articles by Mark Ostwald.

Returning to gas we’ve identified the mechanism at the source of Denniss’ argument – higher export tax lowers domestic prices – is actually just excess supply.

The argument exposes Denniss’ shallow understanding of the physical gas system.

Let’s assume for a moment that the threat of high export taxes would incentivise gas producers to redirect supply to the domestic market. There are two sides to this equation – supply and demand. Where is the supply and where is the demand?

Supply

First we’ll identify logically where the gas must come from for Denniss’ scheme to have any chance of success.

The only gas exports on the Australian east coast are out of Gladstone, the three LNG plants (2 trains each) under various joint ventures with the primary owners Shell, Origin and Santos. The source of the gas is the Surat Basin coal seams in central Queensland (and occasionally further afield when an LNG train is running short!). So Denniss’ redirected export gas can only come from the three Queensland LNG producers.

We’ll put aside for the moment the challenges of a federal government taxing a state resource. PRRT changes in 2019 removed onshore projects from the PRRT and are unlikely to go back in.

There’s plenty of gas in the Queensland ground – nobody disputes that – it’s a fabulous resource that unfortunately is worth zero unless somebody is willing to spend a lot of money getting it out. Lifting costs in the Surat are estimated at $8.50/GJ by the ACCC, including state government royalties. Personal experience says that is a fair estimate.

Source: ACCC gas pricing inquiry

We have established the source of Denniss’ gas is Queensland, therefore it follows the gas must be moved to a market. And where is the primary gas demand in Australia? It’s Victoria….. oh shit!

Demand

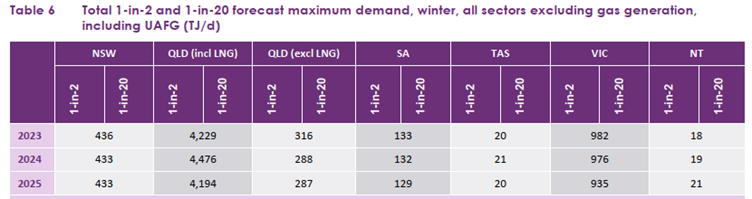

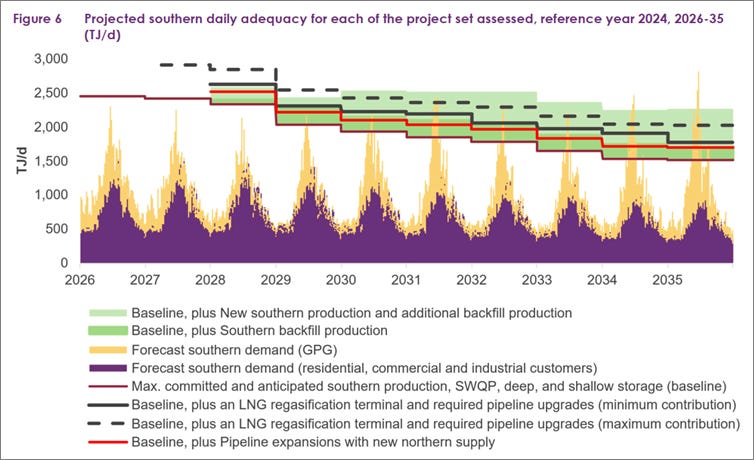

Baseload winter demand in Victoria (excl gas-fired generation) persists above 900 TJ, greater than the sum of all other states in any season.

Add in the gas consumed in power stations during winter and Victorian peak winter gas consumption exceeds 2,000 TJ. At the same time Victorian gas resources are depleting and the crux of all headlines around ‘gas shortages’ becomes this – the pipeline from Queensland is full during winter.

That full pipeline is shown by the red line in the chart below.

Source: AEMO GSOO 2026

Pipes

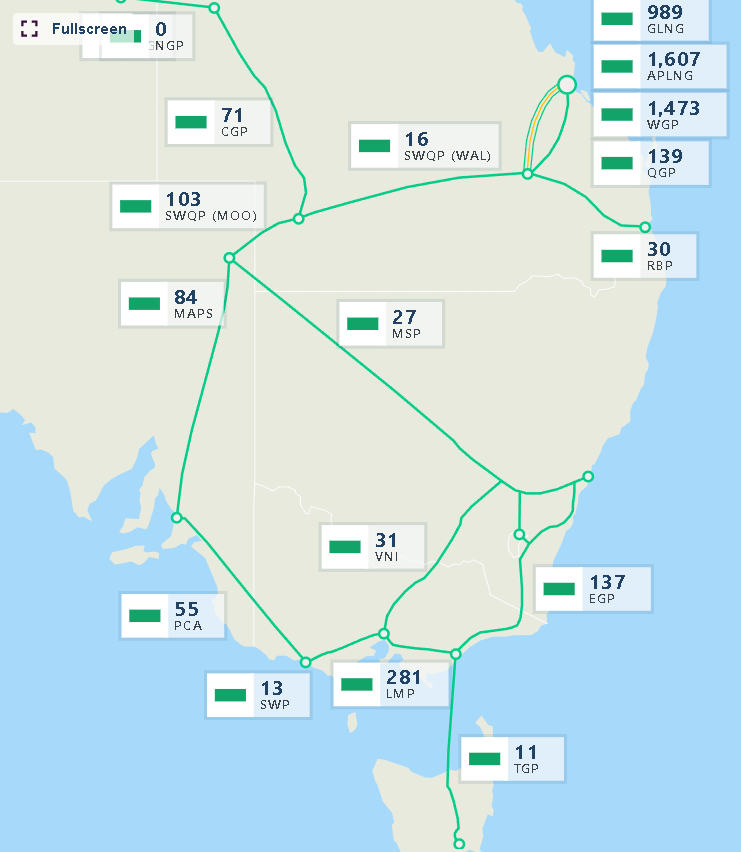

Gas can only get from Queensland to Victoria via the South-West Queensland Pipeline. That pipe has a capacity of 512 TJ/d and length of 937 km.

The southern end of SWQP is Moomba in South Australia where the pipeline is split into the Moomba-Sydney Pipeline (489 TJ/d, 2081 km) and the Moomba-Adelaide Pipeline System (249 TJ/d, 1184 km).

Victoria is downstream of MSP and MAPS through another pipeline from Adelaide to Iona (300 TJ/d, 691 km) or via Culcairn to Wollert (218 TJ/d, 260 km). There’s also the Eastern Gas Pipeline (35 TJ/d, 800 km) linking Sydney to Gippsland and then onto Melbourne via the Longford-Melbourne Pipeline. There are other gas pipes in there, but you get the picture.

Source: https://www.aemo.com.au/energy-systems/gas/gas-bulletin-board-gbb/data-gbb/interactive-map-gbb (the numbers are actual flow rates at the time I took the screenshot).

It is easy to see that the SWQP limits Denniss’ theory of ‘more gas to market’ to 512 TJ/d. Sure there’s storage and other supplies and that all works fine, but the entire Victorian system relies on gas delivered from adjacent Longford, not remote Queensland.

To read more of the gory details try the helpful Victorian Gas Planning Report series by AEMO.

Most people will understand that a pipeline capacity is fixed and can’t be changed without massive cost. Think it’s difficult building a new transmission line over farms? Try convincing people to take a 1m diameter steel pipe full of pure methane 2m below the ground at 9,000 kPag. Consider the cost of getting a pipeline under roads, creeks and across mountains. QGC sold their 500 km export pipeline for $6b in 2014.

If you don’t get the problem with Denniss’ argument by now, let me be clear: gas from Queensland can only get to market in Victoria by pipeline. The pipeline to Victoria is already full in winter. No amount of extra gas can get to Victoria when the pipeline is full.

Ships

What about ships? It is technically possible for gas to be pulled from under the farms of central Queensland, piped at high pressure to Gladstone, converted to LNG, shipped to Melbourne, offloaded through an LNG import terminal and used to offset Victorian peak demand. LNG import terminals are relatively simple facilities and the rest of the infrastructure already exists after all.

Since Denniss’ argument is about cost, let’s analyse the shipping option.

Using ACCC estimates for cost of shipping we get around AUD 1.40/GJ which to be fair is probably cheaper than the tolling charged by the gas pipeline operators. The second cost is the liquefaction which chills the gas until it shrinks to a liquid. LNG is liquid methane shipped at atmospheric pressure.

A typical LNG train is rated around 4 Mtpa and Australia has a total of 22. Six are in Gladstone. Using ACCC numbers we see the cost of piping high pressure gas to Gladstone (1.50/GJ), converting into LNG (6.00/GJ) A LNG import facility would expect to charge a toll (1.00/GJ) bringing the extra cost of shipping LNG to Melbourne approaching 10.00/GJ on top of the lifting cost (8.50/GJ).

So we can see that getting ‘excess gas’ from Queensland to Victoria by ship would incur break-even costs around AUD 18/GJ, far greater than the average AUD 12/GJ seen through 2024 / 2025. Also considering the relatively small volumes (compared to exports) the economics are not in Denniss’ favour.

Another shipping hurdle is cabotage. While foreign ships can carry interstate trade they require special licenses and have to pay the crew Australian equivalent wages while complying with Australian safety regulations and other regulations. Existing cabotage rules would increase the shipping costs further.

Summary

An objective assessment of Richard Denniss’ argument – tax exports to force export gas into the domestic market, therefore lowering gas prices – shows it is logistically impossible, even if gas producers did curtail exports and make that gas available locally. There would be some extra gas sometimes, but it would not be available where it can make a material difference to cost.

Excess supply is still the mechanism that lowers prices, it always has been and always will be.

How about this for a plan: get some gas from Victoria. That eliminates any need for extra pipelines, extra shipping, extra import terminals (all costs). It also provides that extra supply where it’s needed.

Domestic gas will get cheaper if we have more than we need. The mechanism is correct. But extra supply will not be created by extra taxes. Increasing taxation does not increase production.

Denniss’ argument doesn’t stack up.

Finally I ask readers to think about the word ‘fair’. It’s a word bandied about by the activists but there’s nothing more than surface attention given to what it means. There’s plenty to discuss around what exactly is ‘fair’ in terms of royalties.

Why do governments take resource royalties on resources consumed domestically? Doesn’t that mean we pay twice for the use of ‘our’ resources? Is that fair?

I don’t think Richard Denniss and his cronies at the Australia Institute give a fig about fair or reasonable. They are focused on shutting down the resource industries. They know this scare campaign won’t result in higher taxes, but I don’t believe redistribution of gas company revenue is their ultimate aim.

In my opinion the outcome they want is exactly what’s occurring – heaps of attention on gas, lots of misinformation, a witch hunt senate inquiry – all to frighten away new investment and delay planned investment.

Recall this plan for coal: https://www.parliament.qld.gov.au/Work-of-the-Assembly/Tabled-Papers/docs/5516t761/5516t761.pdf

It’s being applied to gas.

Addendum 29/4/2026

A reader comment expressed disagreement that the coal royalty changes had affected QLD coal exports. The QLD government makes all the data public here, called 2025 calendar year—Coal sales statistics:

https://www.data.qld.gov.au/dataset/annual-coal-statistics/resource/c522fcaa-89d7-4c76-bd6e-064d39617d38

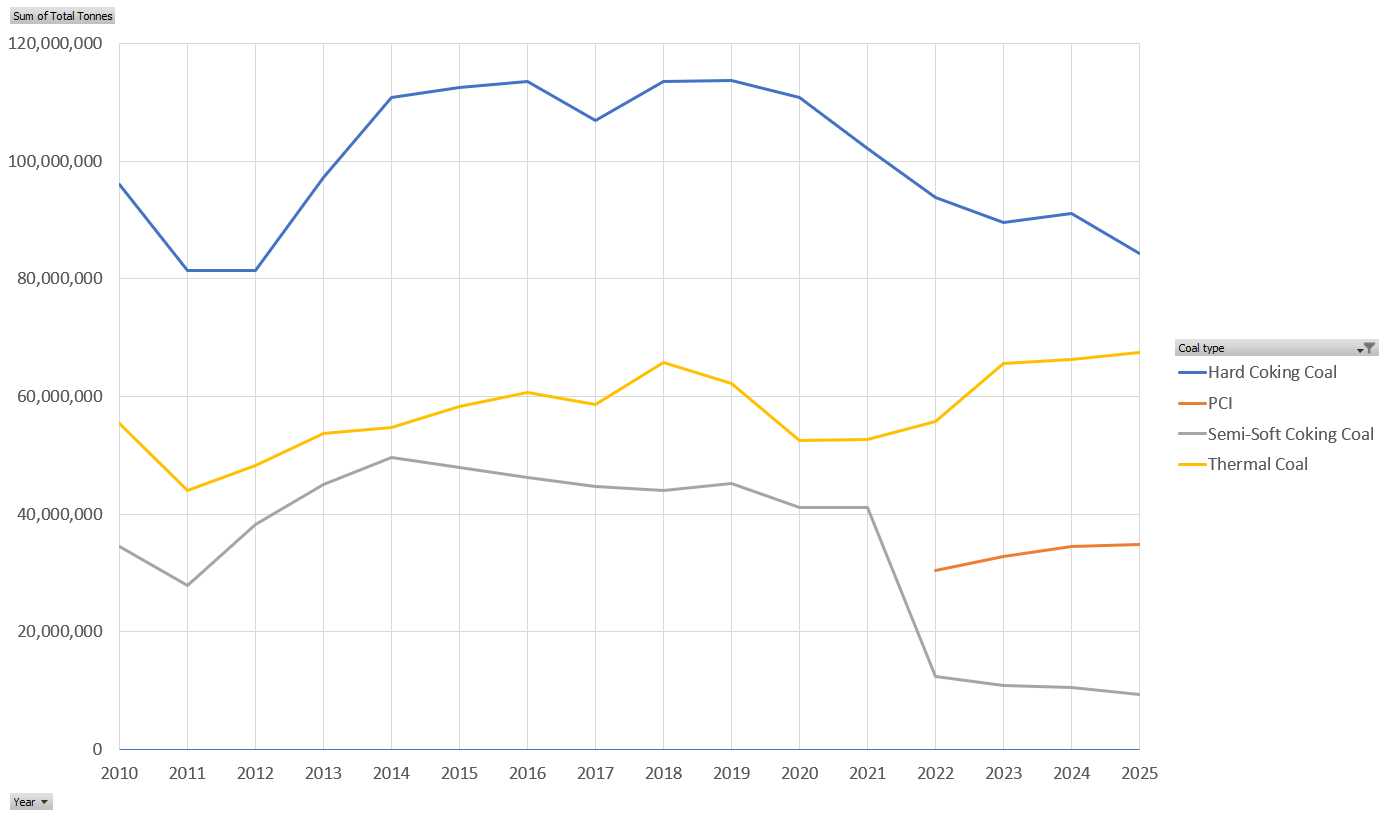

If you download the xlsx file and generate a simple pivot chart you can obtain this graphic showing an overall declining trend in metallurgical coal export tonnes.

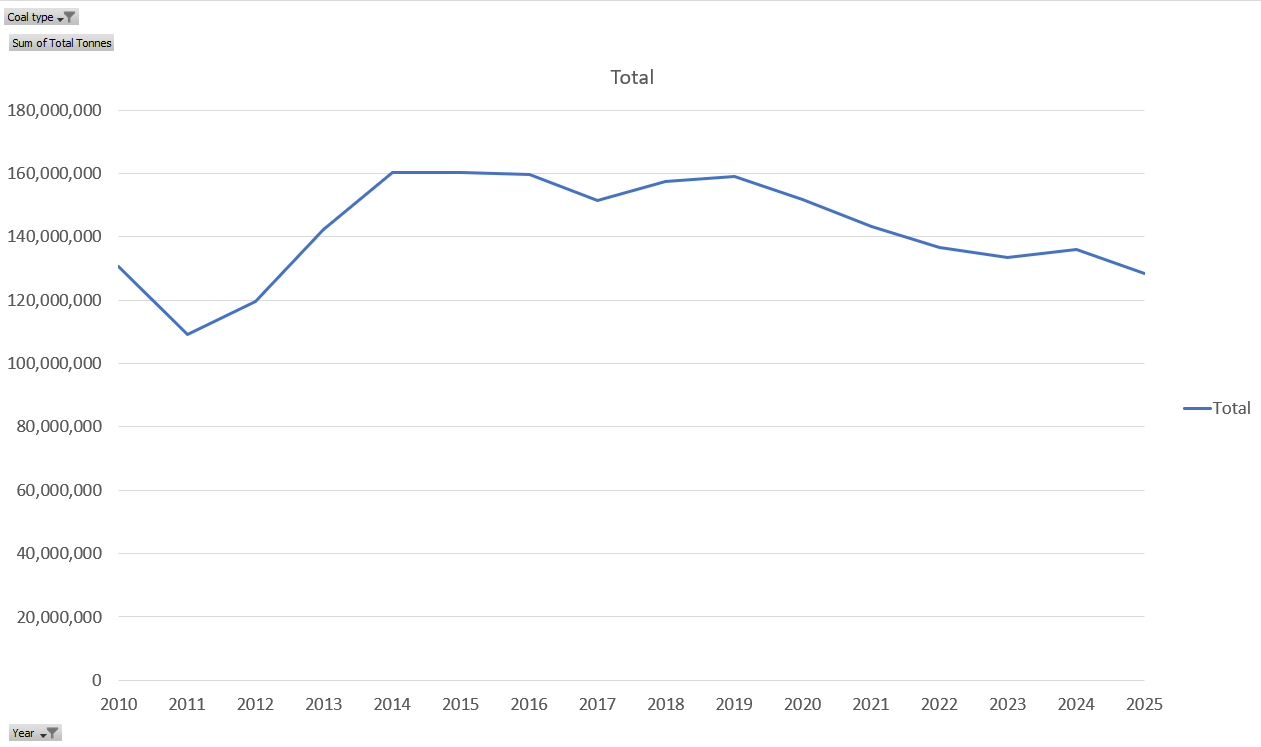

With thermal coal removed the combined metallurgical coal figure is still declining.

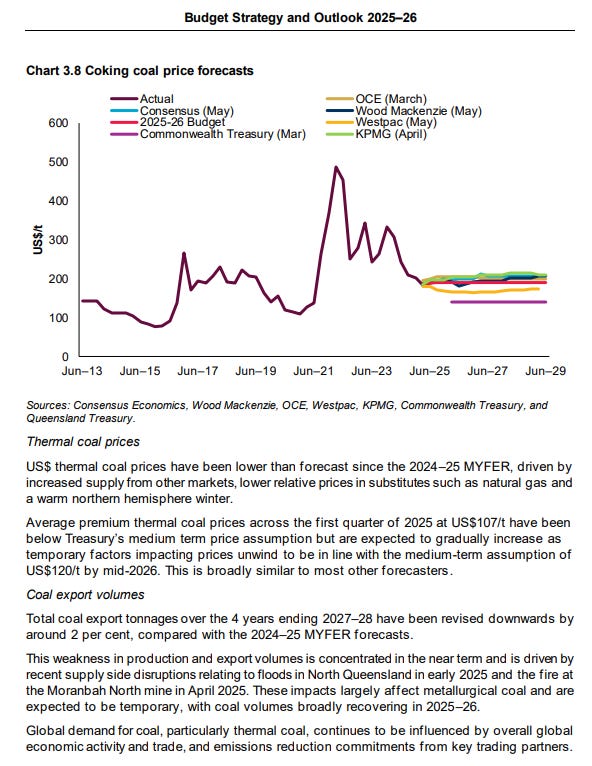

We can look to QLD budget papers for a deeper understanding of the impact from royalties and prices.

https://budget.qld.gov.au/files/Budget-2025-26-BP2-Revenue.pdf

Coking coal prices in the budget are quoted at USD 190/t. Converting by 0.75 we get AUD 253/t, putting met coal squarely in the elevated 30% royalty bracket imposed in 2022.

Therefore I feel it is reasonable to reject Denniss’ claims that higher taxes made no impact on QLD coal mining.

Thank you Ben, this is a masterful expose’ if ever there was one. Australians can safely assume that the political, bureaucratic and deluded-activist classes will scramble into their burrows, rather than read and take on board a factual and incriminating analysis of this standard. It’s not what they want to know, and definitely not what they want the public to know. The best prospect is for the voting public to take this on board, and to vote accordingly.

Brillliant piece Ben. Very well explained.